Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

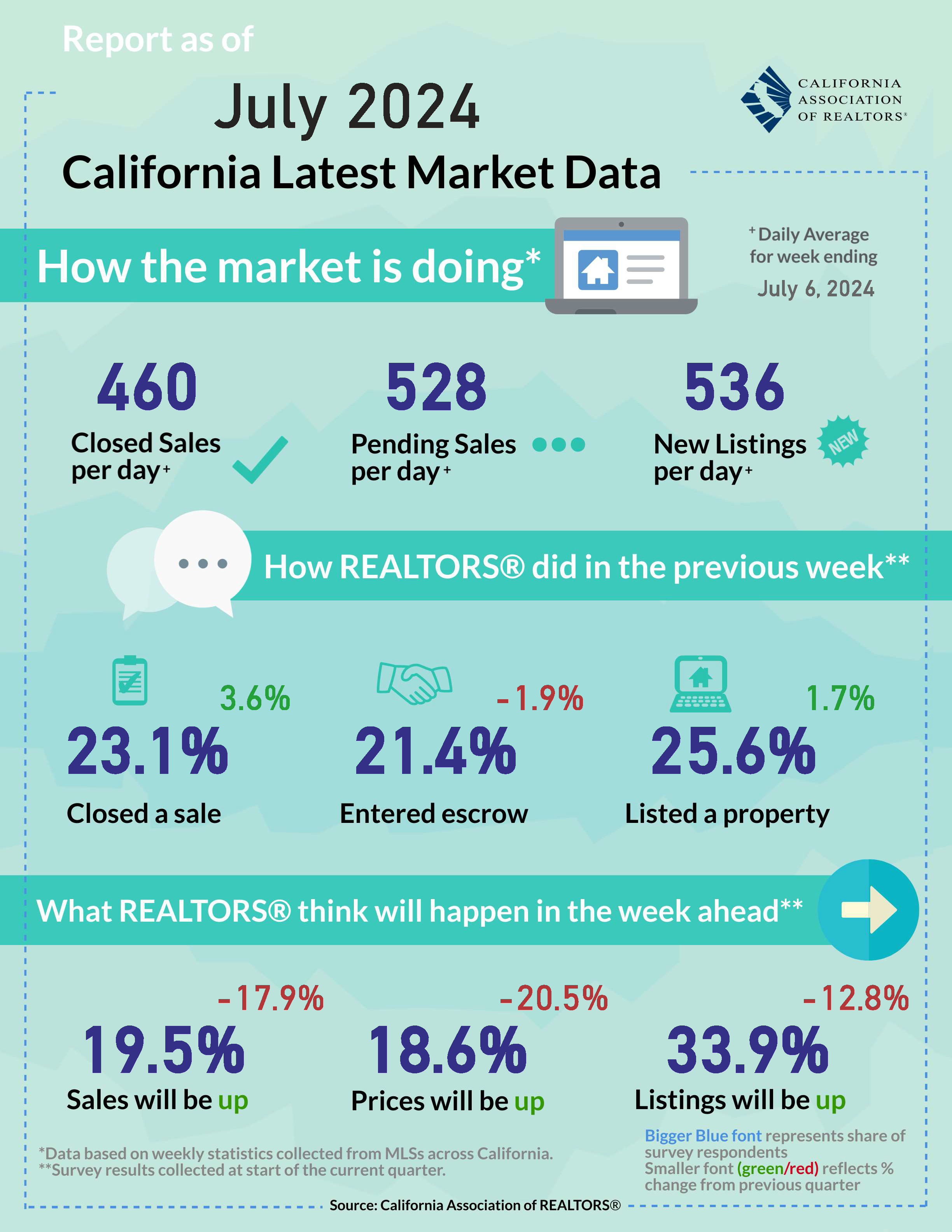

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Watch our C.A.R. economists provide updates on the latest housing market data and happenings... quickly!

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable content.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

REALTOR® Action FundLearn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

July 08, 2024 – The short-term outlook for the housing market looked slightly more positive as interest rates moderated throughout the month of June and the supply condition continued to improve in the past couple of months. With the job market showing signs of cooling in recent weeks and consumers feeling less positive about their future financial well-being, the economy could slow further in the next two quarters. While the growth momentum could be cooling off for the U.S. economy, the housing market could benefit from the slowdown if the Federal Reserve reacts accordingly and starts reducing the policy rates in the near term. Homebuying optimism bounces back: Home Purchase Sentiment released by Fannie Mae bounced back after dipping in May. The share who said that it is a good time to buy increased five percentage points to 19% in June after reaching a survey low of 14% in the prior month. Mortgage rates moderating throughout the month of June provided hope that costs of borrowing could be coming down in the second half of the year and lifted homebuyers’ spirit at least temporarily last month. While those who believed that mortgage rates will decline in the next 12 months dipped slightly from 25% in May to 24% in June, more consumers (79%) felt secured about their jobs last month than the month prior (74%), which could be a reason for the prop-up in homebuying optimism. The share of consumers who said that it is a good time to sell also increased, with a modest climb of two percentage points from 64% in May to 66% in June. The bounce back in home selling confidence will hopefully add more listings to the market and continue to alleviate the imbalance between supply and demand in coming months. Lock-in effect is still in place but fewer homeowners feeling constrained: Housing supply has been slowly improving in the first half of 2024 and the gradual diminishing lock-in effect could be a contributing factor to the increase in inventory. According to data released by Intercontinental Exchange Inc. (ICE) – a financial service company that provides mortgage technology, data and listing services, 76% of homeowners who didn’t own their homes outright had mortgage rates below 5% in May 2024, a drop from 90% recorded two years prior. ICE Mortgage Monitor data indicates that there are 5.8 million fewer mortgages with rates below 5% in the market today than there were at the same time in 2022. With about 4 million mortgages originated with rates above 6.5% since 2022, the share of homeowners with low rates has been declining consistently in the past 24 months. As rates are projected to moderate in the second half of 2024, further improvement in the supply side could be observed before the end of the home buying season. Consumer confidence dips again after a brief rise in May: The Conference Board Consumer Confidence Index edged down in June to 100.4 from 101.3 in May, as consumers remained slightly downbeat about their future economic well-being for the second month in a row. The Expectation Index – a measure that reflects consumers’ short-term outlook for income, business, and labor market conditions – fell last month to 73.0 from 74.9 in May. With the labor market showing more signs of cooling in the past few weeks, Americans’ concerns about future income and business conditions began to weigh on their confidence. While they were more positive about the stock market and less concerned about a forthcoming recession, consumers’ assessment of their family’s current financial situation also weakened in June. Despite fewer expected interest rates to rise over the next 12 months, the share of consumers who planned to purchase a home remained largely unchanged, possibly due to elevated home prices. The sentiment could improve, however, if rates start coming down and prices begin to cool in the second half of 2024. Job growth slows but remains healthy: The U.S. labor market slowed but still added more jobs than expected in June. Nonfarm payrolls increased by 206k jobs last month, a decline from the downwardly revised gain of 218k recorded in May, but the number of newly hired exceeded the 200k projected by the Bloomberg consensus forecast. Most of the job growth was carried by less cyclically sensitive industries, with the health care and social assistance sector gaining 82k jobs and the government employment rising more than 70k. Construction employment growth also remained solid, but most other industries were exhibiting signs of cooling. Meanwhile, the unemployment rate climbed to 4.1% unexpectedly and reached the highest level since November 2021. Wage growth was in line with expectations, with average hourly earnings rising 0.3% month-over-month and 3.9% year-over-year. The annual increase was the smallest since May 2021. The softening in the labor market provides a sigh of relief for the Fed and bolsters the case for the central bank to start cutting the fed funds rate in the fall. Construction spending falls unexpectedly in May: U.S. construction spending fell month-over-month in May, with both residential and nonresidential outlays dropping in the latest report as interest rates remained elevated. The drop of 0.1% from April was the first decrease since October 2022, and the dip was a surprise to economists as the general consensus pointed to an increase before the release of the latest report. On a year-over-year basis, total construction continued to increase 6.4% to $2,139.8 billion. Residential construction edged down in May after an increase in April, with private single-family falling 0.7% month-over-month, while multifamily staying virtually flat from the prior month. High mortgage rates and waning homebuyer traffic were the contributing factors that resulted in a sharp pull back on single-family construction. With interest rates trending upward throughout the month of June, home building activity could decline further in the next couple of months before bouncing back later this year. Note: The weekly market minute report is updated every Monday by 6:00 PM PST.

|

|